If you’re like me, you’re seeing ads for all these new life insurance companies all over the place. Ethos Life Insurance, Ladder, Bestow, Fabric — where did they all come from, and are any of them good enough to trust? How can you compare their rates and pricing, or even compare life insurance policies to begin with? And should you consider any of the old-school providers like MassMutual or Northwestern Mutual? We aren’t getting any younger, so let’s dive into these new life insurance vendors and figure it out.

First, what is life insurance, and who needs it?

The basic concept is pretty simple. When you die, the person (or people) you choose will get paid. You don’t get paid because you are dead, and it’s not like you can take it with you…It’s a win/win for everyone.

Sounds easy enough, but leave it to the finance people to really make it more complicated than necessary. (If you want to skip ahead to the direct comparisons of Ethos, Ladder, Bestow and Fabric, click here)

Types of life insurance

So, from a simple concept to a really complicated reality, there are many, many flavors of life insurance. Just to list out a FEW of the different kinds, you can get:

- Term

- Level Term

- Decreasing Term

- Whole

- Permanent

- Traditional Whole

- Universal

- Variable Universal

- Ok, this is getting ridiculous . . .

The Insurance Information Institute tries to make the different kinds easier to understand in this article, but, in case you don’t have an MBA, here is a bit of a dumbed down primer. You can get one of two basic kinds:

- Term: The policy only lasts for a particular number of years – that period of time is called the “term.” You pay while the policy is valid, and if you die during the policy, hooray, your beneficiaries get paid! (Actually, kind of sad because you are dead.) You stop paying when the policy is over – and again, the policy ends, so no one gets paid.

-

- Whole/Permanent: This policy is more or less designed to last as long as you do. It doesn’t expire in the same way as term does. There are a lot of different kinds of whole life insurance, and since none of the companies we are reviewing in this piece offer it we won’t get into too much detail on the different versions. Suffice to say it gets complicated, because whole is sort of bundled with the ability to build up cash value. I’ve found term premium payments are typically cheaper than whole as well.

Ethos, Ladder, and Bestow offer TERM life insurance

Ethos, Ladder, and Bestow all offer term insurance, not whole life. Why? Term has the following advantages over whole/permanent:

Less expensive

Some sites quote whole life as 6 to 10 times more expensive per month.

Easier to understand

You pick the coverage you want, and how long you want it for; the cost is then shown and there’s no further surprises.

We won’t get into the advantages of whole life insurance now, but there is definitely value for people who want an option to build up cash value.

So who needs term life insurance, anyway?

Should everybody have life insurance? Nope.

Single people without children or dependents usually don’t need it. But, if you’ve got a significant other who you’d like to help protect should you pass, or if you have children (who, it turns out are very expensive!) this kind of protection can be extremely helpful.

Other times single folks may want it for a disabled or elderly person who they take care of, so that there’s money to take care of them in the event of a tragic accident.

An additional use case that single people should consider is if you have cosigned debt, like student loans. Around one in five Americans have student loan debt, and if a parent cosigned your loans they will likely be on the hook to pay them off should you perish.

To summarize, you should consider life insurance if:

- You have kids

- You are married

- You take care of someone else who will need to be taken care of if you die

- Your parents (or someone) cosigned your student loans or other debt

I like term life insurance, since it’s the most basic, easy to understand type of life insurance. There are no strange terminal values or “investment accounts” that you build up over time. Plus it can cost a lot less than whole life. Bestow, Ladder, Fabric, and Ethos offer plain vanilla term life insurance, so let’s compare them.

Comparing Ethos, Ladder, Bestow and Fabric

What are the main differences between Ethos, Ladder, Bestow and Fabric? Each of these life insurance startups has unique takes on signing up, how you get the policy and more. We compare these vendors on terms, high-level cost, financial strength, ease of signing up and more in the table below (further down we’ll have an entire chart dedicated to pricing at each of the providers):

Online Term Life Insurance Comparison | ||||

|---|---|---|---|---|

| Coverage Options | Up to 30 Years | Up to 30 Years | 2, 10 and 20 Years | 10, 15 or 20 Years |

| Ages Covered | 18 – 75 | 20 – 60 | 21 – 54 | 21 – 60 |

| Amount Covered Range | $25,000 to $10,000,000 | $100,000 to $8,000,000 | $50,000 to $1,000,000 | $100,000 to $5,000,000 |

| Simple Term Insurance? | ✅ | ✅ | ✅ | ✅ (except NY, more below) |

| Typical Cost | Above Average | ⭐ Most Competitive | ⭐ Most Competitive | ⭐ Most Competitive |

| Easy to Apply | Very Easy | Pretty Easy | Easiest | Easy |

| Have to Talk to a Sales Person | ❌ | ❌ | ❌ | ❌ |

| Health Check Up Required | ❌ | ❌ No medical exams for coverage up to $3M | ❌ | ❌ |

| Display Price Online | ✅ | ✅ | ✅ | ✅ |

| Issuer | Banner Life Insurance Company | Multiple | North American Company for Life and Health Insurance | Vantis Life |

| Underwriter A.M. Best Financial Strength | A+ | N/A | A+ | A+ |

| Policy Riders | Critical Illness, Child Term, Premium Waivers, Endowment Benefit Rider | ❌ | ❌ | ❌ |

| Convert to Whole Life Option | ✅ | ❌ | ❌ | ✅ |

Length of coverage options

Ethos, Bestow, Ladder and Fabric all offer more than one policy term length, meaning you have choices as to how long you want your policy to last. Ethos and Ladder have policies that last as long as 30 years, while Bestow and Fabric top out at 20 years. In general, as long as you keep making the payments you keep your coverage for the length of the contract.

If you need, or would prefer to get protection for 30 years, concentrate on Ethos Life or Ladder.

Ages for which coverage is offered

Like it or not, the older you get the higher the probability that you pass away. So these insurance companies do not offer policies to folks with a lot of grey hair. Most stop selling new policies to people over the age of 60, although Ethos will sell a new policy to someone as old as 75. If you are over 60, your choice is limited to Ethos, so you might want to go through a traditional broker. And on the younger end, Fabric won’t insure anyone below the age of 21 in most states, while Bestow’s lower limit is 21 everywhere, Ladder is 20 and Ethos goes as young as 18. You should note that if you buy a 20 year policy at the age of 50, your policy will last until you are 70 (assuming you keep paying, of course).

Coverage range

The variety here is pretty amazing. Some of the providers will offer policies as small as $25,000, others only offer ones that are a minimum of $100,000. At the high end the variance is even bigger, with Ethos offering plans as large as ten million dollars (!), and others like Bestow offering plans up to one million dollars. You’ll need to think about how much protection you want to offer your beneficiary; for most people, all of these companies offer a good range of coverage.

What’s the typical cost of term life insurance online?

The cost of each provider deserves its own section, which we have below. Click here to jump to the pricing tables. We’ve rated each vendor based on us filling out their forms and seeing what they offer based on a variety of ages and coverage amounts. You’ve got to applaud these companies for putting their prices right on their website – this is amazing, and a huge step forward in the industry’s transparency.

Since the cost varies by your coverage needs, health, age, location and more it’s hard to generalize about which provider is the lowest cost. However, we roughly rank them as follows, based on the pricing tables we have below:

For the ranking above, we just averaged the cost for each company for all the price points available in our pricing table below. It’s not really a great way to compare the cost of term life insurance – we suggest you read our “how to compare online insurance pricing” section below and price out a few plans yourself. It’s easy to do on these company’s websites.

How easy is it to apply for term insurance online? Do you need a health checkup?

Purchasing life insurance has never been an easy process — until these companies came along. Now, with startups like Bestow and Ladder, you can fill out a few forms and get a policy in a matter of minutes, if approved. With a traditional life insurance company, you typically need to talk to a sales person, fill out forms and — if you are asking for enough coverage — have a visit with a nurse or medical professional for a health checkup. This health checkup may even include getting blood drawn and tested.

If you want to avoid this, the best bet is Bestow, which promises to never have a health check up, or Ladder, which guarantees no medical exams for coverage up to $3M. The others, like Ethos, may require a checkup if the information you provide in your sign up suggest that you “need” one for their underwriting. They say they generally won’t for otherwise healthy people, but it potentially adds an additional step. One of the main reasons you’d go with one of these newer online vendors is to skip the sales call, tedious paperwork and health checkup — all major reasons why these startups are compelling. Fabric tries hard to make it so that you don’t have to do a health checkup, so they score highly on this measure.

Buying life insurance from a traditional vendor is more complicated than you would expect. First of all, you typically have to talk to an agent, who will gather information and generate options for you. Typically, you’ll be required to complete a medical exam as part of the underwriting process, and it may take a couple weeks to receive a decision on coverage.

Thankfully, these new life insurance agencies are making it super fast and easy for you to see your pricing and get a quote in seconds – without having to talk to any sales person (actually, without having to talk to anyone most of the time!)

That being said, if you are just shopping around, you don’t want to have to do a 20 minute health quiz to get a quick price quote, so some of these players are easier than others.

All of these companies offer quick, user-friendly sign up flows. Bestow’s online experience is particularly awesome – hit the “get started” button, fill a single form, see a price quote. All they ask for is gender, birthdate, height, weight, your home state and if you smoke. No contact info or health quiz. Pretty amazing. It’s a great place to start.

Showing the price online

Price transparency earns a major point in our book — the industry is really confusing, it’s hard to understand what you get for what you pay. We LOVE the fact that Bestow, Ladder, and Ethos are open enough to display the cost of their coverage as you fill out their forms.

Fabric’s pricing is also easy to find. In states other than NY, you simply have to fill out a questionnaire before getting to the price.

All about the Issuers

The Issuer (or provider) matters more than you might think. To give you a bit of detail, these startups don’t actually “do” the insurance (nor would you want them to). Instead, they contract with a big, old-school and financially stable life insurance company that takes on the risk and work of paying out to your beneficiaries if you die and your policy is invoked. This is good, because the companies they work with, like MassMutual, Vantis Life, and others are strong companies that should hopefully be around for the length of your contract. These big companies are rated by A.M. Best based on an analysis of their financial position and operating performance. Bestow’s North American Company for Life and Health Insurance has an A+, which is amazingly solid. For the latest ratings, visit www.ambest.com.

The other aspect you need to consider with the underwriter is that this is the company your loved one will have to deal with to get the money, should you die. I think we can all assume they will be pretty shaken up if you pass away, so you want them to be in good hands.

Policy Riders

A couple of these online players give you the option to purchase “policy riders” — basically, for an additional expense, you can customize or “soup up” your policy. Policy Riders = Additional Coverage Options, basically. Only Ethos offers policy riders.

While Ladder does not offer policy riders, they do provide the option for policyholders to adjust their coverage as needs change at no additional cost. If you need more coverage, you can apply to increase your coverage amount. If you need less coverage, for example, after paying off debt or kids graduate from college, you can decrease your coverage amount. Decreasing coverage results in a proportional decrease in premium which can save you money over the life of your policy. Bestow and Fabric have no policy rider options. We’ll update this if the other players do create riders.

Now that we’ve discussed the different features of Ethos, Ladder, Bestow, and Fabric, it’s time to look at how their costs compare.

Comparing the cost of Ethos, Ladder and Bestow life insurance

Ok, time to compare costs – how much does it cost to get term life insurance from Ethos Life, Ladder, Bestow, and Fabric? We break it down in a few different charts below. Remember, there are a lot of different options that can influence the price – your health, your age, your gender, where you live and more. (Oh yeah, and if you are a smoker – guess what, you pay a lot less if you don’t smoke!)

For our analysis, we picked a few different life insurance plans/options and display the price below. Your actual price may vary depending on how you fill out each company’s forms and your individual circumstances, but these charts should be informative of the overall pricing based on a variety of standard factors.

Monthly Life Insurance Pricing for Men

30 year old male | |||||

| 2 / $100,000 | ❌ | ❌ | ❌ | $7.67 | ❌ |

| 10 / $100,000 | $11.00 | $10.15 | $9.55 | $9.58 | $10.78 |

| 20 / $100,000 | $12.00 | $11.10 | $11.56 | $10.25 | $11.53 |

| 30 / $100,000 | $15.00 | $14.98 | $15.66 | ❌ | ❌ |

| 2 / $500,000 | ❌ | ❌ | ❌ | $32.92 | ❌ |

| 10 / $500,000 | $28.00 | $18.50 | $17.26 | $23.33 | $16.25 |

| 20 / $500,000 | $32.00 | $27.35 | $21.47 | $26.25 | $23.56 |

| 30 / $500,000 | $49.00 | $41.92 | $35.07 | ❌ | ❌ |

| 20 / $1,000,000 | $59.00 | $48.71 | $36.78 | $49.16 | $39.16 |

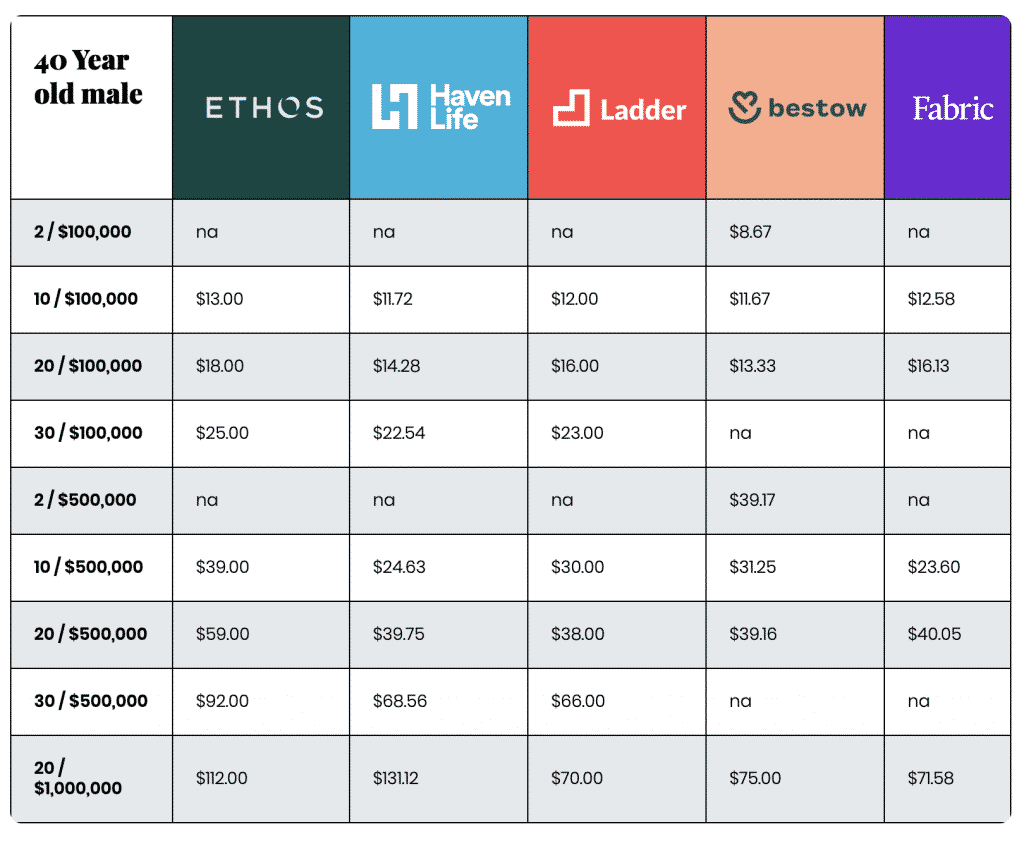

40 Year old male | |||||

| 2 / $100,000 | ❌ | ❌ | ❌ | $8.67 | ❌ |

| 10 / $100,000 | $13.00 | $11.72 | $10.32 | $11.67 | $12.58 |

| 20 / $100,000 | $18.00 | $14.28 | $14.61 | $13.33 | $16.13 |

| 30 / $100,000 | $25.00 | $22.54 | $20.94 | ❌ | ❌ |

| 2 / $500,000 | ❌ | ❌ | ❌ | $39.17 | ❌ |

| 10 / $500,000 | $39.00 | $24.63 | $21.93 | $31.25 | $23.60 |

| 20 / $500,000 | $59.00 | $39.75 | $31.07 | $39.16 | $40.05 |

| 30 / $500,000 | $92.00 | $68.56 | $56.47 | ❌ | ❌ |

| 20 / $1,000,000 | $112.00 | $131.12 | $55.61 | $75.00 | $71.58 |

Prices lists as of 11/19/2021

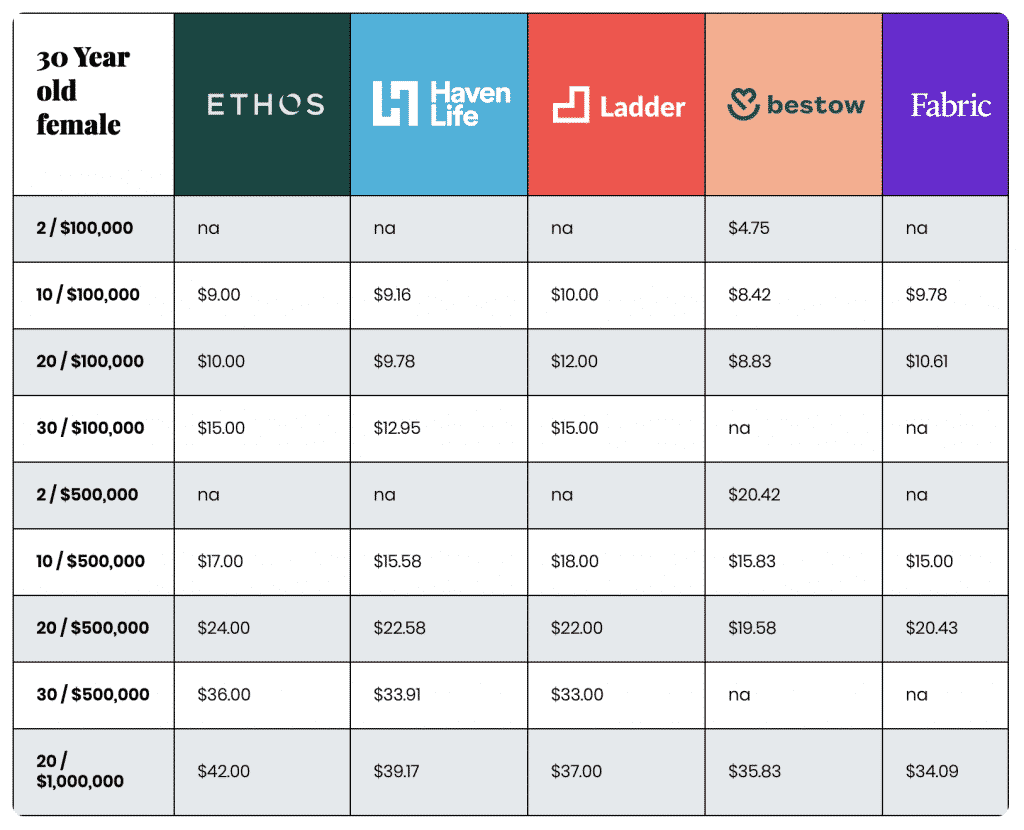

Monthly Life Insurance Pricing for Women

30 Year old female | |||||

| 2 / $100,000 | ❌ | ❌ | ❌ | $4.75 | ❌ |

| 10 / $100,000 | $9.00 | $9.16 | $9.37 | $8.42 | $9.78 |

| 20 / $100,000 | $10.00 | $9.78 | $10.92 | $8.83 | $10.61 |

| 30 / $100,000 | $15.00 | $12.95 | $14.20 | ❌ | ❌ |

| 2 / $500,000 | ❌ | ❌ | ❌ | $20.42 | ❌ |

| 10 / $500,000 | $17.00 | $15.58 | $15.80 | $15.83 | $15.00 |

| 20 / $500,000 | $24.00 | $22.58 | $18.72 | $19.58 | $20.43 |

| 30 / $500,000 | $36.00 | $33.91 | $28.93 | ❌ | ❌ |

| 20 / $1,000,000 | $42.00 | $39.17 | $30.65 | $35.83 | $34.09 |

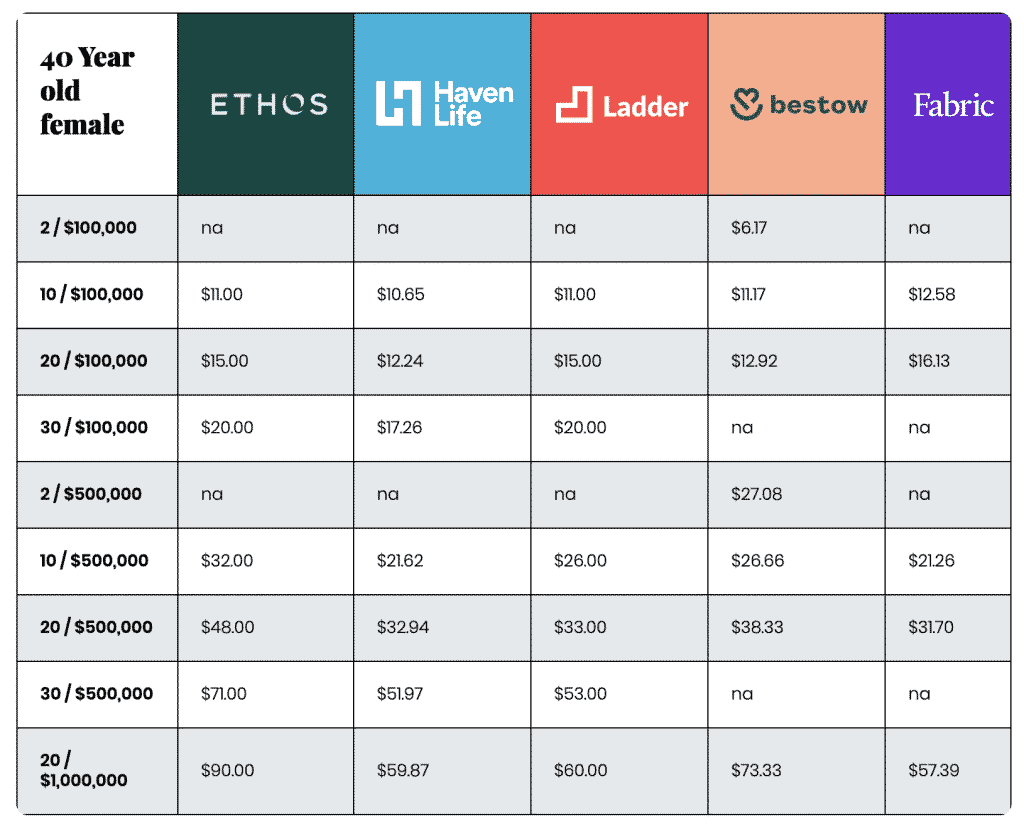

40 Year old female | |||||

| 2 / $100,000 | ❌ | ❌ | ❌ | $6.17 | ❌ |

| 10 / $100,000 | $11.00 | $10.65 | $10.22 | $11.17 | $12.58 |

| 20 / $100,000 | $15.00 | $12.24 | $12.28 | $12.92 | $16.13 |

| 30 / $100,000 | $20.00 | $17.26 | $17.96 | ❌ | ❌ |

| 2 / $500,000 | ❌ | ❌ | ❌ | $27.08 | ❌ |

| 10 / $500,000 | $32.00 | $21.62 | $21.02 | $26.66 | $21.26 |

| 20 / $500,000 | $48.00 | $32.94 | $27.15 | $38.33 | $31.70 |

| 30 / $500,000 | $71.00 | $51.97 | $45.53 | ❌ | ❌ |

| 20 / $1,000,000 | $90.00 | $59.87 | $47.38 | $73.33 | $57.39 |

Prices lists as of 11/19/2021; Fabric and Ladder prices were provided by the company

More detail on how we generated these quotes: We used the websites of Bestow, Ladder and Ethos to quickly and easily come up with the prices listed above. Obviously there are a few questions you have to answer to generate a price quote, and we attempted to use the same criteria to produce these cost charts.

In general, beyond the gender and term/coverage amount listed in the chart, we make the following assumptions: 30 or 40 year olds born on 10/01/1991 and 10/01/1981. Non-smokers. Since a lot of our site visitors are from California, we picked that as the state.

We assumed normal/average height and weights for Americans at the ages picked (source for men, women). Additionally, when asked, we gave our health as “good” or the middle tier, not amazing or bad.

Obviously you may get different life insurance quotes from Ethos, Ladder, and Bestow based on your personal information. The good news is that it’s easy! Learn more about how to comparison shop next.

How to comparison shop for life insurance online

If you are ready to get shopping for life insurance online, we’ve ranked the top online life insurance sites by simplicity, speed and lack of a need to fill out complex, lengthy forms. These three are the best way to compare quotes without submitting your social security number and contact information — yuck! Plus you don’t have to talk to a salesperson, so we recommend you visit these five companies’ websites and get a price comparison:

In our opinion, those are the top online sites. On each, you only have to click a few times to get a quote. They’ll all ask you for your age, location and a few other, basic questions before giving you a price estimate. Bestow even promises to never give you a health checkup (something that is possible, but rare with Ethos.) As we mentioned earlier, with Ladder, there are no medical exams for coverage up to $3M.

So go for it, use the links above to see how much it might cost you! We’ve ranked Bestow and Ladder as our favorites, because their online forms look like this – all on a single page:

How to get a Bestow Life Insurance Quote

Bestow insurance quoter

Ethos makes you push a few more buttons, but the basic questions are the same. Again, super simple and fast – and no contact or personal information required.

Fabric Life Insurance Online Price Quoter – start here!!

Fabric has a great price quoter tool that you can access here. This tool is great for getting a quick price estimate – just enter your age, sex, state, if you smoke and your general health. I wish it was easier to estimate your Fabric Life Insurance price quote directly from their home page — so instead of starting there, start with the price quoter!

Ok, now let’s get to our recommendations.

The Verdict: Which do we recommend, Bestow, Ethos, Ladder, or Fabric life insurance?

So what’s our opinion on the right online life insurance for you? All of these companies are price competitive, with Ladder, Fabric and Bestow offering the best prices for the segments we reviewed — 30 to 40 year old men and women looking for coverage between $100,000 to $500,000.

If you need one million dollars worth of coverage, Ladder generally takes the cake as well. Ethos generally offers the best coverage for those over 60, or anyone needing more than $1m in coverage.

But it’s not just about price — since none of these companies actually issue the policy, you are also forming a relationship with the underwriter that they’ve chosen to work with. That provider needs to be stable, and also should be known as being fair to work with (should you pass away, you want your beneficiaries to be working with a company with a positive reputation and proven history of paying claims. Because of that, we like Bestow, Ladder, and Fabric best.

Finally, which is easiest to get going with? You are shopping online for a reason, right, you shouldn’t have to deal with salespeople or agents. And if you can avoid having to be seen by a doctor or nurse to get your health checked out, even better. For that reason, we love Ladder and Bestow’s online user interface most – you can get a quote in seconds, and the fact that they don’t require health checkups (up to $3M and $1.5M, respectively) is a huge plus.

As we mentioned above, Ethos also has a great online experience, and it’s worth filling out their simple forms quickly to see the cost if you want to shop around. And you can use the Fabric price quoter to quickly see if you can get some of their great pricing.

In summary, we recommend you get a quote from ALL the providers — Ladder, Ethos, Bestow, and Fabric. Luckily these companies make it fast and painless to do so, which may not always be the case with traditional insurance companies. While we’ve provided the general contours that set these companies apart, ultimately, without complete visibility into your full situation and needs, we can’t say 100% which will be most effective for your family.

More nerdy low cost online life insurance stuff

Want more info on the low cost online life insurance brands Bestow, Fabric, Ethos, and Ladder? Keep reading – we’ll compare these companies below.

Bestow vs Ethos

Which life insurance provider is better, Bestow or Ethos? As we explained above, both offer simple online forms that quickly give you a price quote. Bestow’s life insurance company is North American Company for Life and Health Insurance, and has an A+ financial strength rating from A.M. Best. Ethos works with Banner Life Insurance Company, which also has an A+ rating, and is known as a company who is easy for your beneficiaries to work with. Comparing the pricing of Bestow vs. Ethos, Bestow has slightly lower prices for men aged 30 and 40 looking for $100,000, $500,000 to $1,000,000 in coverage at a variety of terms. For example, based on the pricing in our charts above, a 20 year, $500,000 policy for a man is $26.25 with Bestow and $32 with Ethos. Unless you need policy riders, want a 30 year term, or want the option to convert your term insurance to whole life, Bestow is probably better. If you’re over 6o or need a plan with a ton of coverage (up to $10m), go with Ethos.

Ladder vs Ethos

Both Ladder and Ethos offer term life insurance policies up to 30 years in length. In our opinion, Ladder and Ethos have some of the simplest online pricing, meaning it’s fast and easy to get a price quote. Ethos offers policies to people aged 18 to 75, while Ladder is for people 20 to 60. Both offer wide ranges in policy sizes; Ethos will provide policies from $25,000 to $10,000,000 and Ladder can go from $100,000 to $8,000,000.

As our pricing chart above shows, Ladder is more affordable for both men and women, for nearly all the segment we priced out. For women, both offered 40 year old women 10 year, $100,000 policies for around $11 per month. Ladder’s million dollar policies seem to be more affordable. Ethos farms out their policy underwriting to a third party company, whereas Ladder controls their own underwriting process. Ladder also has the benefit of flexible coverage allowing policyholders to decrease or apply to increase their coverage over the life of their policy.

Comparing low cost online term life insurance vs traditional insurance companies

How do the online providers compare against the traditional life insurance providers? First of all, Ethos, Ladder, and Bestow don’t require you to talk to an insurance agent or commissioned sales person, AND they have great websites that can quickly estimate your price after you answer just a few questions. Plus, Ladder, Ethos, and Bestow don’t typically make you do a health checkup with a doctor or nurse, which is better than many of the traditional vendors. If you are interested, here are the largest life insurance companies in the United States who you might know about:

- Northwestern Mutual

- Lincoln Financial

- New York Life

- MassMutual

- Prudential Financial

- John Hancock

- State Farm

- Transamerica

- Pacific Life

- MetLife

How does the pricing of leading online life insurance companies Ethos, Ladder, and Bestow compare to the cost of insurance from a traditional vendor? Well, it’s not typically very easy to figure out what the cost of a big vendor is, because you usually have to go through a live insurance agent to get a price quote.

The ability to get a price online without talking to anyone is a key advantage of the players like Ethos, Ladder, and Bestow. Below, we compare the price of a 20 year, $100,000 policy for a 30 year old male in California in good health between Bestow, Ladder, Ethos and Fabric, a well-known, traditional life insurance provider:

You can see the pricing is much lower with the online vendors. As we mentioned above, the pricing for Bestow, Ladder, and Ethos is super easy to get online, so we recommend getting a few quotes to see what kind of coverage makes the most sense for you.

Methodology

We conduct extensive research to evaluate the pricing, effectiveness, accessibility, overall quality, and user experience of every telehealth service we review. This also includes examining and comparing each provider to comparable telemedicine alternatives. We also evaluate usability, treatments, prescription delivery time, and more to determine the best value for those seeking fast and reliable telehealth services.

| Review Process | Key Metrics | Weighting |

|---|---|---|

| Sign up online | – ease to complete intake form – affordability – upfront commitment or subscription required? – money back guarantee or refund policy? | 0.5 |

| Vitual consult with provider / determine eligibility | – ease to get appointment to determine eligibility – need to leave house for labs or other in-person care? | 1 |

| Shipping + unboxing | – shipping cost – time from order to treatment delivery – discreet packaging to maintain privacy | 0.5 |

| Test + journal for 1-3 months | – ease of application – transition into habitual use – taste / smell / feel / pain | 1.5 |

| Results after 3 months of use | – efficacy / results – lack of side effects – ease of refill / reordering – quality of ongoing clinical support – responsive customer support – willingness to recommend to a friend | 1.5 |